SMM September 1 News:

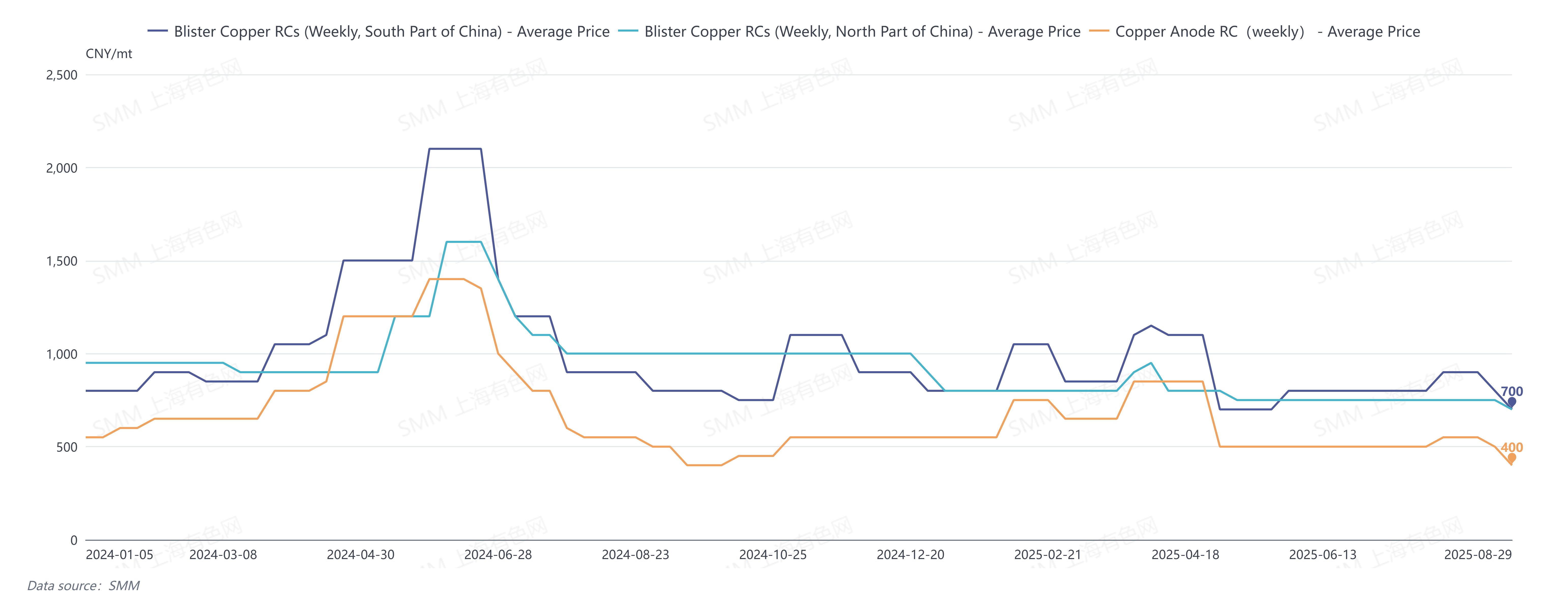

In August 2025, SMM quoted blister copper RCs in south China at 750-950 yuan/mt, averaging 850 yuan/mt, up 50 yuan/mt MoM. Blister copper RCs in north China were quoted at 650-850 yuan/mt, averaging 750 yuan/mt, flat MoM. Blister copper RCs CIF China were quoted at $90-100/mt, averaging $95/mt, unchanged MoM.

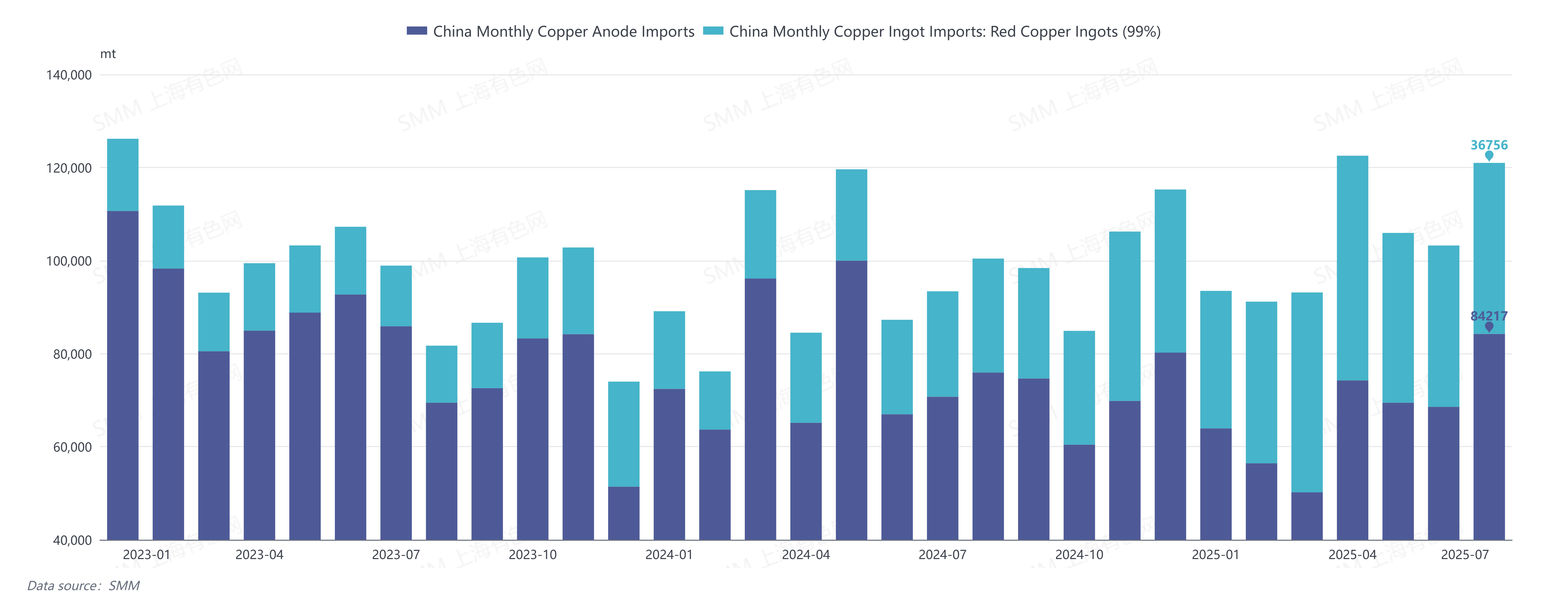

In August, blister copper RCs in south China rebounded slightly, mainly due to high inventory levels at some smelters and relatively weak demand that month. Meanwhile, increased arrivals of imported copper anode supplemented market supply. Customs data showed China imported 84,200 mt of copper anode (HS code: 74020000) in July 2025, up 22.86% MoM and 19.08% YoY. Imports of copper scrap ingots (red/purple copper ingots, HS code: 74031900) reached 36,800 mt, up 6% MoM and 62% YoY. However, due to maintenance at ore-derived blister copper suppliers and tight supply of recycled copper raw materials, the domestic supply landscape remained tense.

Nevertheless, uncertainties stemming from policies in the secondary copper industry may drive RCs to hit bottom again in September.

On August 29, SMM weekly blister copper RCs in south China were quoted at 600-800 yuan/mt, averaging 700 yuan/mt, down 100 yuan/mt WoW. Weekly blister copper RCs in north China were quoted at 600-800 yuan/mt, averaging 700 yuan/mt, down 50 yuan/mt WoW. Weekly blister copper RCs CIF China were quoted at $90-100/mt, averaging $95/mt, flat WoW. Copper anode plate processing fees were quoted at 350-450 yuan/mt, averaging 400 yuan/mt, down 100 yuan/mt WoW.

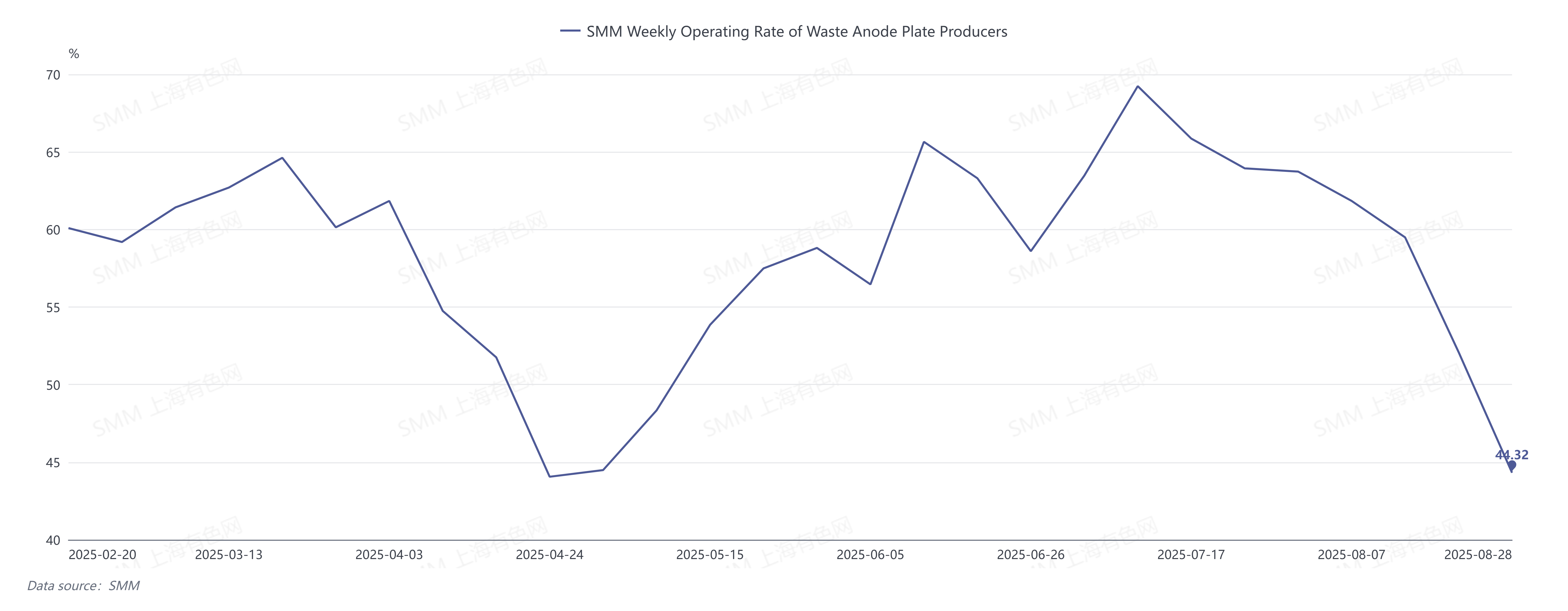

Supply side, policies regulating investment incentives in the secondary copper industry targeted local governments' cleanup of illegal subsidies and tax rebates, increasing tax burdens for secondary copper smelters and processing enterprises. Additionally, environmental protection inspections in some regions before September 3 led to varying degrees of production cuts or shutdowns. SMM data showed the weekly operating rate of scrap-derived anode plate producers dropped sharply by 7.78 percentage points WoW to 44.32% during August 22-28. Although enterprises with long-term contracts could temporarily rely on raw material inventories to maintain production and fulfill deliveries, overall supply of blister copper and anode plates is expected to decline significantly amid tight recycled copper raw material supply and high procurement costs.

Demand side, as September and October will enter the concentrated maintenance period for smelters, companies increased stockpiling demand for copper anode to minimize production losses of copper cathode. Meanwhile, given concerns over further supply contraction after the clarification of secondary copper policies, some smelters began advance inventory buildup. With expectations of significant supply decline and persistently robust demand, the supply-demand imbalance in the blister copper and anode market is projected to worsen further.

The implementation status of the "Notice on Regulating Investment Promotion Activities and Related Policy Implementation Matters" (NDRC System Reform [2025] No. 770) will directly affect domestic production of scrap-derived anode plates, thereby impacting copper cathode output. SMM estimates the operating rate of smelters not using copper concentrates (utilizing copper scrap or anode plates) at 59.9% in September, down 8.3 percentage points MoM.